International

A.T. Kearney expects debt-driven oil and gas shakeout

Depressed oil prices will force oil and gas companies in distress to seek scarce buyers in a debt-driven shakeout, according to A.T. Kearney’s Oil and Gas M&A Outlook. The report, which was released recently reveals that 2016 will be a pivotal year for all oil and gas companies as they look to complement their aggressive capex and cost reductions with divestitures, mergers, and acquisitions.

Globally, companies with weak balance sheets will be forced to offload assets and seek partners to support their cash position as funding options dry up, while companies in a stronger financial position will have the opportunity to capture reserve and merger synergies.

“There will be ample opportunities for potential buyers, and we expect to see a surge in assets and companies up for sale,” said Richard Forrest, A.T. Kearney’s global lead partner for the Energy Practice and co-author of the report.

“Despite the drop in oil prices since mid-2014, the low-cost Gulf producers remain largely profitable. However, continued fiscal pressure will push many countries and their national oil companies to focus on internal operational efficiency and economic diversification rather than large-scale international M&A. With the increased focus on value and job creation as well as diversification, new partnership opportunities will arise for international players,” said Ada Perniceni, partner, A.T. Kearney.

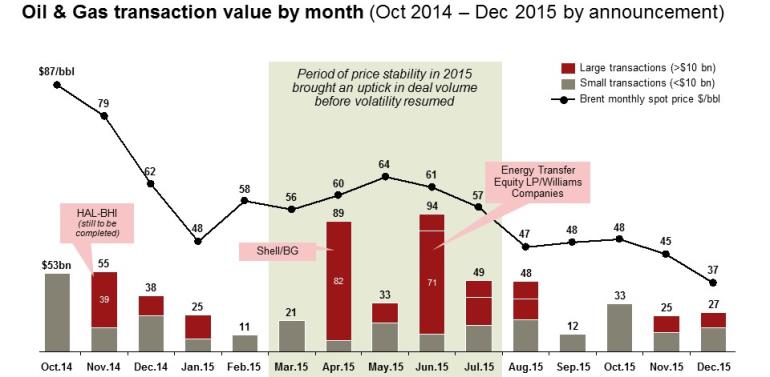

In 2015, oil and gas M&A activity was limited with only a few major deals dominating headlines such as Royal Dutch Shell’s $81.5 billion acquisition of BG Group. Midstream deal value rose by 68 per cent, with the Energy Transfer Equity–Williams deal in the lead. Master limited partnerships (MLPs) largely contributed to this increase, making up well over half the total deal value.

However, total upstream deal value declined by 13 per cent; if the impact of the outsized $81.5 billion Shell–BG deal in 2015 is excluded, total upstream deal volumes dropped by 54 per cent. Oil field services total deal volume declined 61 per cent, and with the exception of the Cameron International–Schlumberger transaction, the top 10 deals involved financial investors rather than incumbent firms within the industry purchasing oil and gas assets.

Recent price volatility has created sharp differences in valuation expectations between buyers and sellers, delaying M&A decisions. Companies are focusing on cash preservation and cost reductions but are quickly exhausting options and now have to dig deeper and structurally change their strategies.

This year will be a pivotal one as cash and liquidity concerns drive a shakeout for those with high costs and debt, the report said. Operators with high debt holdings, especially those relying on reserve-based lending, could see their funding squeezed and credit facilities reduced, triggering them to shed low-performing assets.

This will present opportunities for those willing and able to adopt contrarian strategies and take advantage of creative deal structures. M&A deals—whether acquiring, partnering, or divesting—will be a vital way to grow value, cut costs, and navigate the new, more turbulent landscape.

“There are limited buyers today, but the current situation represents a huge opportunity for those with the financial strength required,” said Alvin See, A.T. Kearney principal and co-author of the report.

“Companies, including selected national oil companies (NOCs), may capitalize on the current climate to secure reserves or expand operations, and financial investors are busily gearing themselves up for deals. Any run-up in oil prices lasting a couple of quarters will likely be met with a flurry of deals.”

Stronger independents will have the opportunity to acquire assets at a deep discount as debt covenants and redeterminations will play a larger role in triggering M&A. Financial investors will also seek opportunities to put capital to work, targeting different levels of return through varied M&A approaches.

International oil companies (IOCs) will focus on structural cost reduction and portfolio high-grading, making selective acquisitions and continuing divestment programs, especially in unconventional resources, more likely than mega-mergers. BP, Chevron, and Shell, for example, have announced over $45 billion in combined asset sales over the next few years.

The report forecasts that geopolitics will have a major impact on M&A activity as fiscal austerity will limit M&A in the Middle East, while in China opportunistic oil and gas M&A will play well into Xi Jinping’s “One Belt, One Road” vision. In addition, 2016 will bring consolidation as smaller companies become targets or start to consider creative financing options.

“The year ahead will require tough decisions and a survival mind-set for many non-competitive operators,” Richard Forrest concluded. “For those willing to think and strategize creatively, 2016 will be transformational for individual companies and the long-term future of the industry.”

{kind=link}

Sohar International Contributes OMR100,000 to Support Those Affected by Al Masarrat Weather Conditions

Liva Insurance Announces New CSR Initiative to Renovate Children’s Cancer Ward at Sultan Qaboos University Hospital

Real Estate Price Index in Oman Grows By 13.9%

Oil Surges More Than 2% as Supply Disruptions Mount

Ibri Industrial City Localises Two Projects Worth RO2M in 2025

VIDEO: Al Khamayil Oman Scales Up Production with New Rusail Facility

Cadillac Enhances Ramadan Ownership Value With Premium Benefits Package

CONNECT and OCEC Partnership Strengthens Oman’s Position as a Global Events Destination

Exclusive: Inside Oman’s Evolving MSME Finance Ecosystem – An Interview with Hussain Al Lawati, CEO, Development Bank

Middle East Tensions Heighten Risks to Strait of Hormuz, Raising Uncertainty for Global Oil Markets

Power And Beyond: The Path To A Low-carbon Future

Al Mouj Muscat unveils Ghadeer Villas

Time to Buy Saudi Stocks? Some Investors Look at Dubai Instead

Renewables are booming, but not fast enough to cap greenhouse emissions

Hospitality Industry in Oman Estimated 90% Growth in 2022

Retail Abu Dhabi’s ‘Unbox Amazing’ generates sales of more than AED 2 billion in participating stores

Saudis Sign Deals From Energy to Metals in Bid to Salvage Forum

Saudi Arabia’s Gold Miner Plans to Be a Global Top-20 Supplier

Technology to drive Sultanate’s downstream industry

Digitization and Logistics Service Providers Can Help SMEs Make the Most of Peak Season Retail Trends

VIDEO: Robert MacLean on how NHI is Shaping Oman’s Next Generation of Hospitality Leaders

The Future of Oman: Decoding The Sultanate of Oman’s Strategic Promotional Nation Brand

EXCLUSIVE: AI, Robotics & Wearable Sensors are Changing the Lives of Dementia Patients

EXCLUSIVE: Talking Renewable Projects & Sustainability in Oman and Beyond with Vipul Tuli

VIDEO: Eng. Salim Al Thuhli, CEO, Khazaen Economic City on Investment Opportunities

H.E. Salim Al Aufi, Minister of Energy & Minerals talks about Oman’s Green Hydrogen Goals

VIDEO: Talking Latest Developments in Aircraft Ground Guidance & More at Oman Airports

VIDEO: Dr. Firas Al-Abduwani Discusses Green Hydrogen, Potential Regions for Development & Creating a Green Ecosystem

VIDEO: Discussing The Future of Green Hydrogen in Oman with H.E. Salim Al Aufi

Celebrating Infoline’s Remarkable 20-Year Journey

-

Dossier1 month ago

Dossier1 month agoDossier, 2026

-

OER Magazines1 month ago

OER Magazines1 month agoOER, February 26

-

Banking & Finance1 month ago

Banking & Finance1 month agoSohar International and Sohar Islamic Supports Over 100 Families in Al Wusta Governorate Through Its ‘Sohar Al Attaa’ Initiative

-

Banking & Finance1 month ago

Banking & Finance1 month agoNational Finance Unveils Exclusive Ramadan Offers on Auto Financing

-

Economy1 month ago

Economy1 month agoAnalysis: Oman-India CEPA Opens Path to Deeper Trade Investment and Growth

-

Economy1 month ago

Economy1 month agoMiddle East Tensions Heighten Risks to Strait of Hormuz, Raising Uncertainty for Global Oil Markets

-

Economy1 month ago

Economy1 month agoANALYSIS: Oil Near Seven-Month Highs Amid US, Iran Tensions

-

Economy1 month ago

Economy1 month agoNew Regulations Issued for Buy Now, Pay Later Services in Oman

You must be logged in to post a comment Login